Your credit report is the single most important document defining your financial opportunities, from apartment rentals to loan rates. Yet, errors are surprisingly common—and they can silently, significantly hurt your score.

A mistake on your report is essentially a financial lie about you, and leaving it uncorrected means accepting a lower financial standing than you deserve. At SmartDwell, we encourage everyone, especially renters building their financial foundation, to regularly review their reports. If you find an inaccuracy, knowing these three simple, powerful steps will allow you to correct it and ensure your score reflects your true financial health.

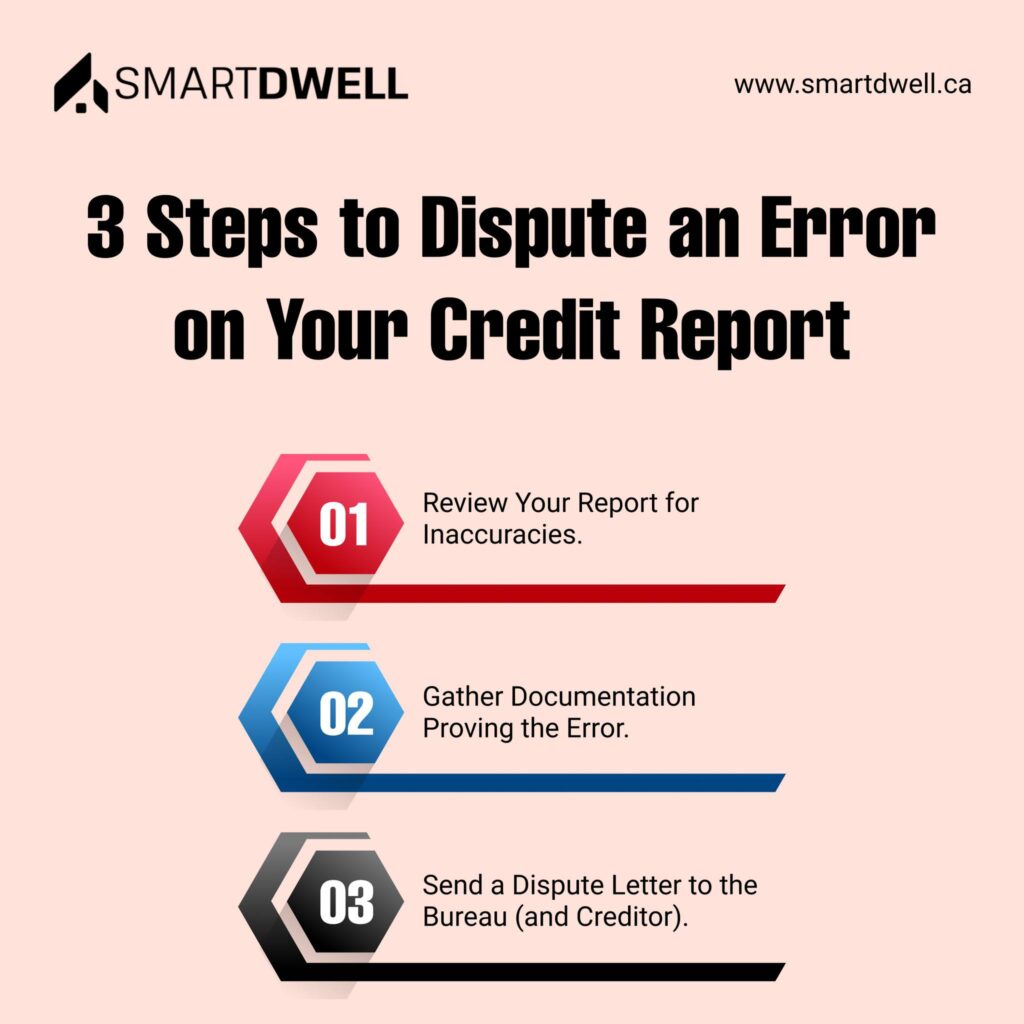

Step 1: Review Your Report for Inaccuracies

The first step is vigilance. You are entitled to a free copy of your credit report from the major credit bureaus annually. Don’t just glance at the numbers; read every line item with a critical eye.

Look for common mistakes, such as:

- Identity Errors: Wrong name, phone number, or social security number.

- Account Errors: Accounts that are not yours, closed accounts listed as open, or the same debt listed multiple times.

- Reporting Errors: Incorrect payment dates, wrong balance amounts, or payments you made on time incorrectly listed as late.

Spotting the error is the necessary first action in protecting your financial reputation.

Step 2: Gather Documentation Proving the Error

Once you’ve identified the mistake, you need to become your own best financial advocate by compiling clear evidence. The credit bureau and creditor will only remove the item if you can prove it is incorrect.

Your documentation should include:

- Copies of canceled checks or bank statements showing the payment was made on time.

- Account statements showing a zero balance on a debt listed as current.

- Copies of correspondence with the creditor that acknowledges the error.

- A highlight on your credit report showing exactly which item is inaccurate.

This evidence is the ammunition for your formal dispute.

Step 3: Send a Dispute Letter to the Bureau (and the Creditor)

Do not rely on online forms alone, especially for complex errors. The most effective way to dispute an error is by sending a formal, detailed letter via certified mail (requesting a return receipt). This creates a clear, legal paper trail.

Your dispute package should include:

- A formal dispute letter clearly stating the error, explaining why it is wrong, and requesting its removal or correction.

- Copies of all your supporting documentation (never send originals).

- A copy of your credit report with the disputed item highlighted.

Crucially, you should send a copy of the letter and documentation to the creditor (the company that reported the mistake) as well as the credit bureau. This is often called a “dual dispute” and ensures both parties are aware of the issue and obligated to investigate.

The bureau generally has 30 to 45 days to investigate and respond. By taking these three clear, documented steps, you take powerful control of your financial data and ensure your credit score reflects your true financial health.